CA Intermediate Syllabus 2021 and CA Inter Exam Pattern 2021

CA Intermediate Exam Pattern 2021: In India, the CA Intermediate exam is the second level of the Chartered Accountancy test. It consists of eight disciplines and about 7000 pages of study material that an understudy must complete in the nine months allotted to them. The gathering structure is what makes this test significantly more difficult, as a gathering consists of four subjects, and a competitor must pass each of the four papers to pass the gathering.

The failure to pass one topic swiftly causes the entire group to be disappointed, implying that the understudy fails in the subjects in which he has passed. It should be noted that the average dropout rate from the year 2000 to 2020 was only 16.76 percent, implying that only 16 out of every 100 students who took the test were able to pass it. As a result, the greatest un-passing rate in the November 2018 Chartered Accountancy Course in India was only 8.88 percent. Understudies in the wake of clearing the Common Proficiency Test (CPT) or CA Foundation Course become qualified to enroll for the CA Intermediate. On the other hand, graduates, postgraduates, or understudies having equal degrees can directly get enrolled for the CA Intermediate exam without appearing for the passage level tests.

CA Intermediate Syllabus New Course Updates 2021

ICAI has made changes in the CA transitional prospectus for May 2021 test. ICAI has added some new themes and diminished some old points from the ICAI prospectus. Given below are some of the modifications in the CA transitional Syllabus done by ICAI for the May 2021 assessment.

Addition of Topics in the CA Inter Syllabus 2021

All the updates which are made by the ICAI for the Nov 2021 test are mentioned below:

Accounting subjects of paper 1 have been shifted to paper 5 progressed bookkeeping.

ICAI has added disintegration of Partnership firms including piecemeal dispersion of resources alongside the change of organization firm into an organization and deals with an organization which is an issue identified with bookkeeping in restricted obligation association.

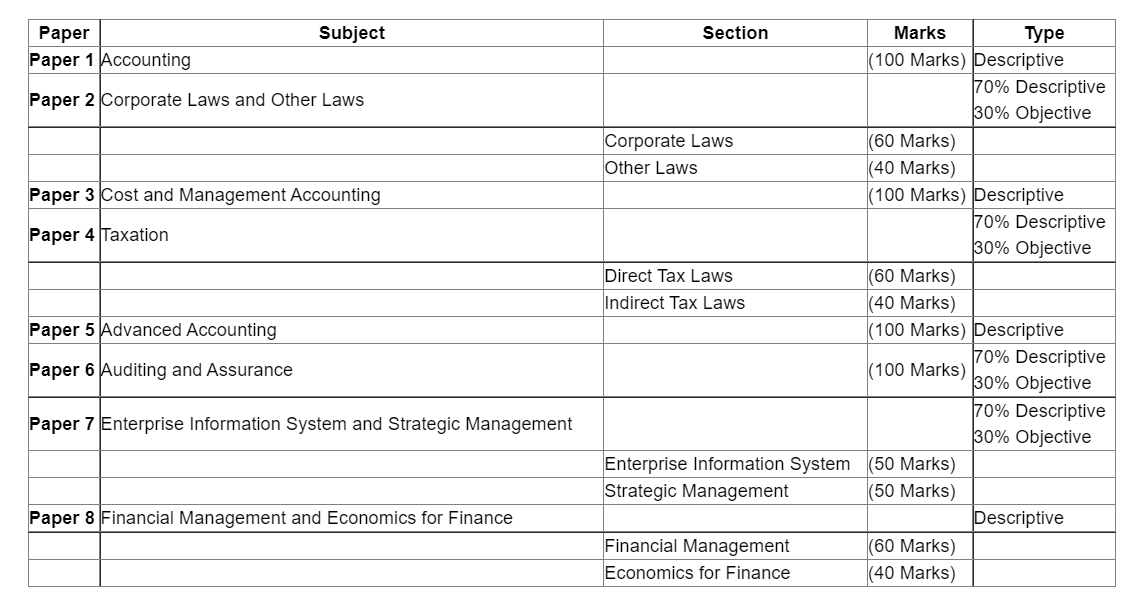

Subjects and the marks distribution of the CA Intermediate New Course are:

CA Intermediate Syllabus For Paper 1– ACCOUNTING

Chapter | Chapter Names |

1 | Process Of formulation Of Accounting Standards including Ind ASS (IFRS converged standards) and IFRSs; convergence vs adoption; Objective and concepts of carve-outs |

2 | Framework for Preparation and Presentation Of Financial Statements (as per Accounting Standards) |

3 | Applications of Accounting Standards |

4 | Company Accounts |

5 | Accounting for Special Transactions |

6 | Special Type of Accounting |

CA Intermediate Syllabus For Paper 2– CORPORATE AND OTHER LAWS

Part I: Corporate Law

Chapter | Chapter name |

1 | Preliminary |

2 | Incorporation of Company and Matterds Incidental thereto |

3 | Prospectus and Allotment of Secunt1es |

4 | Share Capital and Debentures |

5 | Acceptance of Deposits by Companies |

6 | Reg1strabon of Charges |

7 | Management andAdministration |

8 | Declarabon and Payment of Dividend |

9 | Accounts of Companies |

10 | Audit and auditors |

We hope you found the information presented in this post to be helpful. Wishing you the best of success with your next examinations! Continue reading about this topic CA Intermediate Syllabus and Exam Tip’s.

CA Intermediate Online Classes are available at Takshila Learning Students can choose between the best online and offline classes, Check out CA Intermediate exam date and CA Intermediate registration fees on Takshila Learning Portal for more information on CA Intermediate Course Call us at 8800999280/83/84 and Book a CA Intermediate Demo Class Now.

Comments

Post a Comment

Thank you we will contact ASAP.